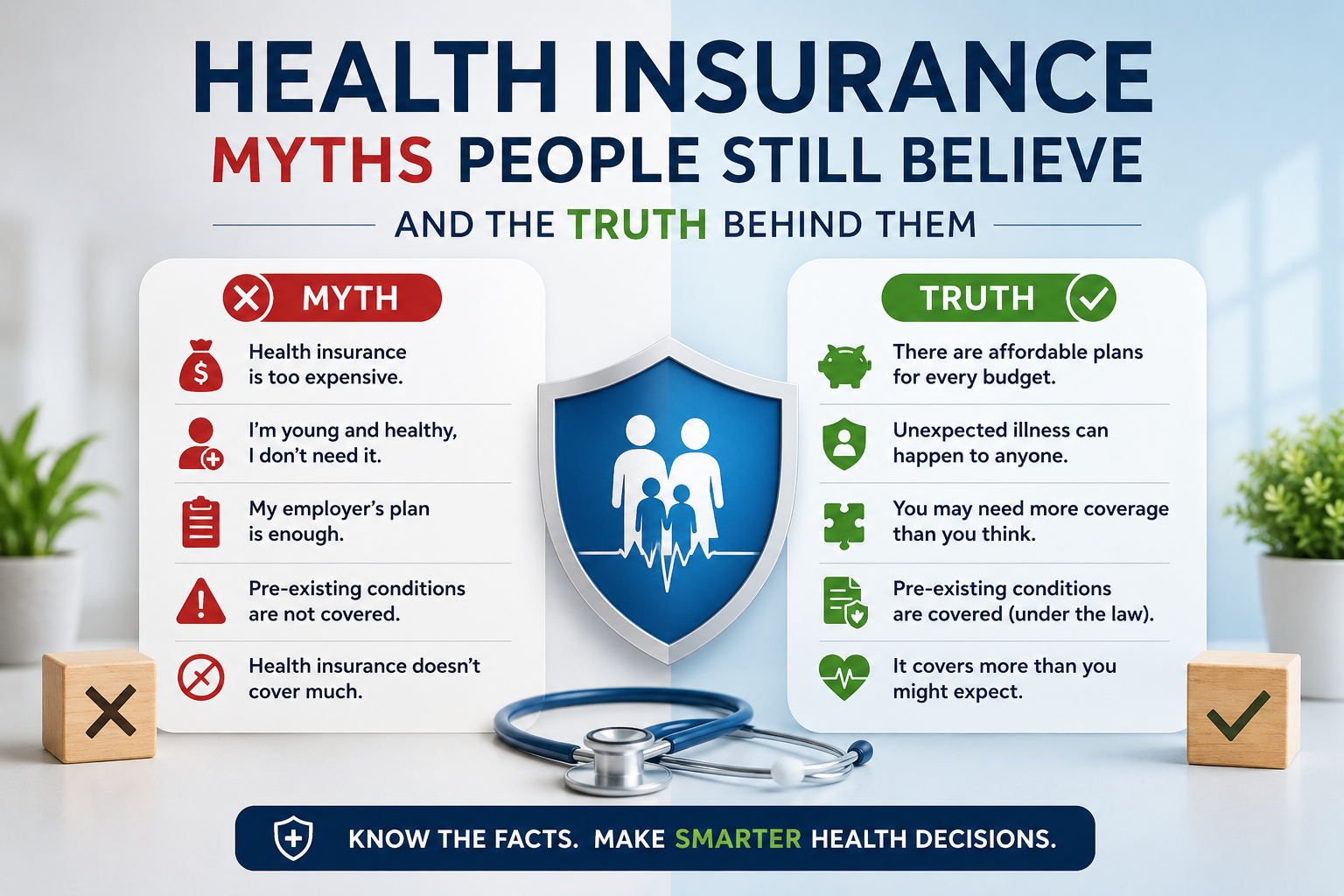

Health insurance is one of the most important financial tools you’ll ever use — yet it’s also one of the most misunderstood. From assuming you don’t need it when you’re young and healthy to thinking your employer’s plan is always the best deal, millions of people make costly decisions based on outdated or flat-out wrong information.

These myths don’t just cause confusion. They lead to surprise medical bills, missed benefits, and gaps in coverage that can seriously hurt your finances. In this article, we break down the most common health insurance myths still circulating today, backed by facts — so you can make smarter, more informed choices about your coverage.

Myth #1: “I’m Young and Healthy, So I Don’t Need Health Insurance”

This is probably the most dangerous myth of all. The logic sounds reasonable — why pay monthly premiums for something you never use? But here’s the problem: no one plans to get sick or injured.

A single ER visit can cost anywhere from $1,500 to over $10,000 depending on the treatment. A broken leg, a sudden appendicitis, or a car accident doesn’t check your age before it happens. Without coverage, you’re one bad day away from serious medical debt.

The truth: Health insurance isn’t just for sick people. It’s a financial safety net that protects you from unexpected, high-cost events. Even a healthy 25-year-old benefits from preventive care, mental health services, and emergency protection.

Myth #2: “Health Insurance Covers Everything After I Pay My Premium”

Many policyholders believe that once they’re enrolled, all medical costs are handled. This is one of the most persistent health insurance misconceptions out there — and one of the most expensive to discover the hard way.

Most health plans include several layers of cost-sharing:

| Cost Type | What It Means |

|---|---|

| Premium | Monthly payment to maintain coverage |

| Deductible | Amount you pay before insurance kicks in |

| Copay | Fixed fee per visit or service |

| Coinsurance | Your percentage share after the deductible |

| Out-of-Pocket Maximum | The cap on what you’ll pay in a year |

Some treatments — particularly elective procedures or experimental therapies — may not be covered at all. Always read your Summary of Benefits and Coverage (SBC) document carefully.

Myth #3: “The Cheapest Plan Is the Most Affordable Option”

It feels logical: lower monthly premium = more money in your pocket. But this thinking ignores a critical part of the equation — your total annual healthcare costs.

Low-premium plans almost always come with higher deductibles, higher copays, and narrower provider networks. If you have even a moderate health need during the year, what you save on premiums can easily be wiped out — and then some — by higher out-of-pocket costs.

How to compare plans properly:

- Estimate your typical annual healthcare usage

- Add up premiums + expected deductible + copays

- Compare that total across plan options, not just the monthly rate

- Factor in whether your preferred doctors are in-network

Myth #4: “My Employer’s Plan Is Always the Best Choice”

Many employees assume their workplace plan is automatically the right fit — after all, the employer pays a portion of it. But employer-sponsored plans vary enormously, and they may not align with your personal healthcare needs.

If your employer offers a high-deductible plan, you might actually save more by shopping on the Health Insurance Marketplace and applying for subsidies — especially if your household income qualifies. There is no law that forces you to enroll in your employer’s plan.

Consider comparing your employer plan against marketplace options if:

- Your income qualifies for Affordable Care Act (ACA) tax credits

- Your employer’s plan has a limited provider network

- Your plan doesn’t cover specialists or medications you regularly use

Myth #5: “Pre-Existing Conditions Mean I Can Be Denied Coverage”

This myth was once true — but it hasn’t been since 2014. Under the Affordable Care Act (ACA), insurance companies are legally prohibited from denying coverage or charging higher premiums based on pre-existing conditions such as diabetes, asthma, heart disease, or cancer.

Whether you’re buying through the marketplace or through an employer, your health history cannot be used against you in any plan that falls under ACA regulations.

The truth: You have the right to comprehensive coverage regardless of your medical history. If someone tells you otherwise, verify your rights directly at HealthCare.gov or with a licensed insurance broker.

Myth #6: “Health Insurance Is Only for Physical Illness”

This outdated belief leads many people to avoid seeking mental health treatment, assuming it won’t be covered. In reality, the Mental Health Parity and Addiction Equity Act (MHPAEA) requires most health plans to cover mental health and substance use disorder services at the same level as physical health services.

Most modern health plans cover:

- Therapy and counseling sessions

- Psychiatric evaluations and medication management

- Substance use disorder treatment

- Behavioral health programs

If you’ve been avoiding mental health care because you assumed it wasn’t covered, it’s worth calling your insurer to review your actual benefits.

Myth #7: “Health Insurance Doesn’t Cover Preventive Care”

Many people avoid annual checkups, screenings, or vaccines because they assume they’ll face a bill afterward. Under the ACA, most health insurance plans are required to cover a wide range of preventive services at zero cost to you — no copay, no deductible.

Preventive services typically covered at no cost include:

- Annual wellness exams

- Blood pressure and cholesterol screenings

- Mammograms and cervical cancer screenings

- Vaccines and immunizations

- Diabetes prevention programs

- Mental health and depression screenings

Taking advantage of these covered benefits is one of the best ways to get real value from your policy.

Myth #8: “Using My Insurance More Will Raise My Premiums”

This myth likely comes from the car insurance world, where filing multiple claims can increase your rates. Health insurance works very differently. Using your health benefits — for doctor visits, prescriptions, or specialist care — does not increase your premium.

Your health insurance premium is determined by factors like your age, location, tobacco use, and the plan tier you choose. It is not based on how frequently you use medical services during the year.

Myth #9: “I Don’t Need Health Insurance Because I’m Covered by a Family Member’s Plan”

Being listed as a dependent on a spouse’s or parent’s plan sounds reassuring — but there are important limitations to understand. Young adults are only eligible for coverage under a parent’s plan until age 26. After that, independent coverage is necessary.

Additionally, even while on someone else’s plan, you should understand:

- Which providers are in-network for you

- Whether the plan covers your geographic area if you live in a different state

- What happens to your coverage if the primary policyholder changes jobs or loses coverage

Having a backup plan or understanding your rights to enroll in your own plan protects you from sudden gaps in coverage.

Myth #10: “Self-Employed People Can’t Get Affordable Health Insurance”

Freelancers, independent contractors, and small business owners often believe they’re locked out of affordable coverage. This simply isn’t accurate.

Self-employed individuals can:

- Shop for plans through the ACA Marketplace (HealthCare.gov)

- Qualify for income-based premium tax credits and cost-sharing reductions

- Deduct health insurance premiums from their taxable income

- Join professional associations that offer group health plan access

In many cases, a self-employed person with moderate income can find a solid plan for well under $100/month after applying available subsidies.

Quick Reference: Myths vs. Facts

| Health Insurance Myth | The Real Fact |

|---|---|

| Young and healthy people don’t need it | Anyone can face sudden illness or injury |

| Insurance covers all costs | Deductibles, copays, and coinsurance still apply |

| Lowest premium = most affordable | Total annual costs matter more than monthly premium |

| Employer plans are always best | Marketplace plans may offer better value |

| Pre-existing conditions lead to denial | ACA prohibits this practice |

| Mental health isn’t covered | MHPAEA mandates mental health parity |

| Preventive care costs money | Most preventive services are free under ACA |

| Using insurance raises premiums | Health plan premiums are not usage-based |

| Self-employed can’t get affordable plans | Marketplace subsidies are widely available |

Conclusion

Health insurance myths don’t just spread misinformation — they cost people money, prevent them from accessing care, and leave them financially exposed when they can least afford it. The more you understand how your plan actually works — from deductibles and copays to covered preventive services and your rights under the ACA — the better positioned you are to make decisions that protect both your health and your wallet.

Don’t let myths make your healthcare decisions for you. Review your plan documents, use your preventive care benefits, and speak with a licensed insurance broker if you’re unsure whether your current coverage truly fits your needs.

Frequently Asked Questions (FAQs)

Does health insurance cover pre-existing conditions?

Yes. Under the Affordable Care Act, insurers cannot deny coverage or charge more based on pre-existing conditions.

Is mental health covered under standard health insurance plans?

Most plans are legally required to cover mental health and substance use disorder services at parity with physical health benefits.

Can self-employed people get health insurance subsidies?

Yes. Self-employed individuals can apply for ACA premium tax credits based on their income through HealthCare.gov.

Does using health insurance frequently raise your monthly premium?

No. Health insurance premiums are not affected by how often you use your medical benefits during the year.

Are preventive care visits free with health insurance?

Under the ACA, most preventive services — including annual checkups, screenings, and vaccines — are covered at no cost to the enrollee.

What’s the difference between a deductible and a premium?

Your premium is what you pay monthly to keep coverage active; your deductible is the amount you pay out-of-pocket for care before your insurance starts sharing costs.

Can I opt out of my employer’s health insurance plan?

Yes. There is no law requiring you to enroll in an employer plan. You can shop for alternative coverage on the marketplace if it better fits your needs.

What happens to my coverage when I turn 26 and age off my parent’s plan?

You qualify for a Special Enrollment Period, giving you 60 days to enroll in your own health insurance plan through your employer or the marketplace.