Health insurance comes with a language all its own. If you’ve ever stared at your insurance card or Explanation of Benefits (EOB) and felt completely lost, you’re not alone. Terms like deductible, copay, and coinsurance show up on nearly every health plan — yet most people don’t fully understand what they mean or how they interact.

Getting these terms straight isn’t just an academic exercise. It directly affects how much money comes out of your pocket every time you visit a doctor, fill a prescription, or go to the hospital. This guide breaks down each term in plain language, shows how they work together, and helps you make smarter decisions when choosing or using your health plan.

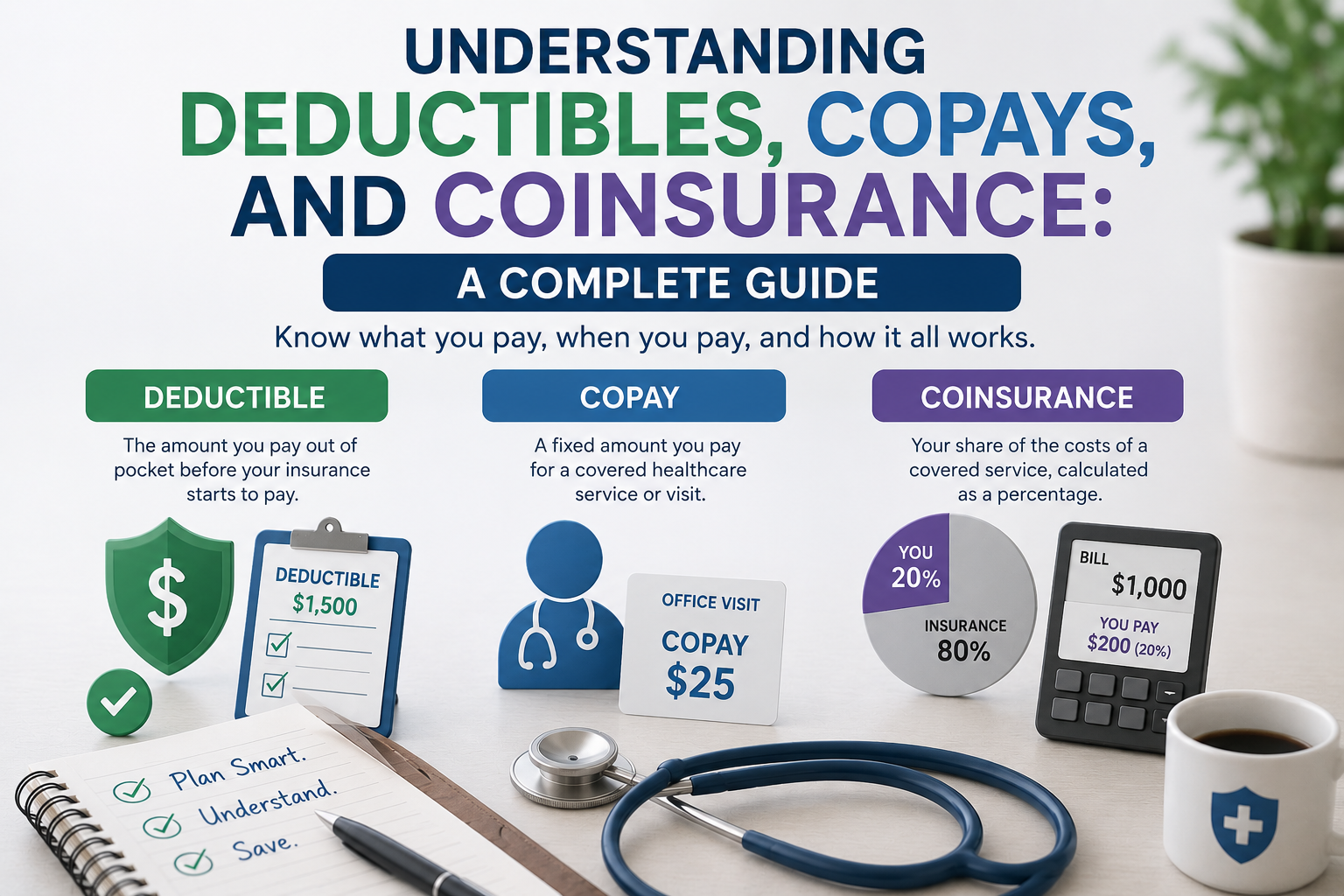

What Is a Deductible?

A deductible is the amount you pay out-of-pocket for covered medical services before your insurance company starts sharing the cost. Think of it as the “entry fee” to your insurance coverage.

For example, if your annual deductible is $1,500 and you have a medical bill of $2,000, you pay the first $1,500 yourself. After that, your insurance steps in to cover a portion of the remaining $500.

Key Facts About Deductibles

- Deductibles reset at the start of every plan year (usually January 1st or on your policy anniversary date)

- A higher deductible generally means a lower monthly premium, and vice versa

- Individual and family plans have separate deductible amounts

- Some services — like preventive care — may be covered before you meet your deductible

- In-network providers almost always have a lower deductible threshold than out-of-network providers

High Deductible Health Plans (HDHPs) pair well with Health Savings Accounts (HSAs), making them a smart option for generally healthy people who want to save on premiums while building tax-free medical savings.

What Is a Copay?

A copay (short for copayment) is a fixed, flat fee you pay for a specific healthcare service at the time you receive it. Unlike a deductible, copays kick in immediately — you don’t need to meet any threshold first.

For example, your plan might charge:

- $25 for a primary care physician visit

- $50 for a specialist appointment

- $10–$20 for a generic prescription

- $250 for an emergency room visit

Key Facts About Copays

- Copays are predictable — you always know the amount in advance (often listed on your insurance ID card)

- They typically apply to office visits, urgent care, and prescriptions

- Copays usually do not count toward your deductible, but they do count toward your out-of-pocket maximum

- Not all health plans use copays — some use coinsurance exclusively

- Copays reset annually with your plan year

Because copays are a fixed amount, they’re one of the most straightforward costs in health insurance. You show up, hand over your copay, and you’re covered for that visit.

What Is Coinsurance?

Coinsurance is the percentage of a covered medical bill that you pay after you’ve already met your deductible. It’s a cost-sharing arrangement between you and your insurance company.

The most common split is 80/20, meaning your insurer pays 80% and you pay 20% of eligible costs.

How Coinsurance Works: A Real Example

Let’s say you have a $1,000 deductible and 20% coinsurance, and you receive a $5,000 medical bill:

- You pay the first $1,000 (your deductible)

- Of the remaining $4,000, your insurance covers 80% = $3,200

- You owe 20% = $800 as coinsurance

- Your total out-of-pocket cost: $1,800

Key Facts About Coinsurance

- Coinsurance only applies after your deductible is met

- The percentage you owe can differ for in-network vs. out-of-network care

- It continues until you reach your out-of-pocket maximum

- Common splits include 70/30, 80/20, and 90/10

Quick Comparison: Deductible vs. Copay vs. Coinsurance

| Feature | Deductible | Copay | Coinsurance |

|---|---|---|---|

| What it is | Annual amount you pay first | Fixed fee per service | Percentage you pay after deductible |

| When it applies | Before insurance shares costs | At time of service | After deductible is met |

| Amount type | Fixed dollar amount | Fixed flat fee | Percentage of bill |

| Counts toward deductible? | Yes | Usually no | N/A |

| Counts toward OOP max? | Yes | Yes | Yes |

| Resets | Annually | Annually | Annually |

The Out-of-Pocket Maximum: Your Financial Safety Net

No guide on deductibles, copays, and coinsurance is complete without covering the out-of-pocket maximum (OOP max). This is the absolute ceiling on what you’ll pay for covered in-network services in a single plan year.

Once you reach this limit — through any combination of deductible payments, copays, and coinsurance — your insurance covers 100% of covered costs for the rest of the year.

For 2024 ACA marketplace plans, the out-of-pocket maximum cannot exceed:

- $9,450 for individuals

- $18,900 for families

What Does NOT Count Toward Your OOP Max?

- Monthly premium payments

- Costs for services not covered by your plan

- Out-of-network charges (on most plans)

- Balance billing amounts from out-of-network providers

How Deductibles, Copays, and Coinsurance Work Together

Understanding each term individually is useful, but the real picture emerges when you see how they function as a system throughout your plan year.

Here’s a typical journey through a plan year:

- January (Plan year starts): Your deductible resets to $0. Every covered service you use starts chipping away at it. You may pay copays for routine visits right away.

- Mid-year (Deductible met): After enough doctor visits, lab work, or a major procedure, you’ve hit your deductible. Coinsurance now kicks in — your insurer starts sharing costs.

- Later in the year (OOP max reached): After enough coinsurance payments stack up, you hit your out-of-pocket maximum. Your insurance now pays 100% of all covered services for the rest of the year.

- January again: Everything resets. The cycle begins anew.

Tips for Choosing the Right Plan Based on These Costs

When comparing health insurance plans during open enrollment, don’t just look at the monthly premium. Consider these factors together:

- If you’re generally healthy: A high-deductible plan with lower premiums may save you money, especially paired with an HSA

- If you have chronic conditions or expect surgery: A lower deductible with higher premiums might cost less overall due to frequent care

- If you take regular prescriptions: Check the copay tiers for your specific medications before choosing a plan

- If you have a family: Look at both individual and family deductible thresholds — family plans often have both

- In-network matters: Always check that your preferred doctors and hospitals are in-network before enrolling

Frequently Asked Questions (FAQs)

Does my copay count toward my deductible?

In most plans, copays do not count toward your deductible, but they typically do count toward your out-of-pocket maximum.

What happens after I meet my deductible?

Once your deductible is met, your insurer begins sharing costs — you’ll either pay coinsurance (a percentage) or copays, depending on the service.

Is coinsurance the same as a copay?

No. A copay is a flat fee (e.g., $30), while coinsurance is a percentage of the total bill (e.g., 20%) that you owe after your deductible is met.

Do deductibles reset every year?

Yes. Most deductibles reset at the start of each new plan year, which is often January 1st for employer-sponsored plans.

Can I have both a copay and coinsurance on the same plan?

Yes — many plans use copays for routine visits and coinsurance for larger or specialized services, sometimes both for the same category depending on the service.

What is a $0 deductible plan?

A plan with no deductible means your insurance starts sharing costs from your very first covered service, though premiums are typically higher to compensate.

Does my deductible include prescription costs?

It depends on your plan. Some plans have a separate prescription deductible, while others fold medications into the general medical deductible.

Conclusion

Deductibles, copays, and coinsurance are the three core building blocks of how you share healthcare costs with your insurer. Your deductible is what you pay first; copays are flat fees for specific services; and coinsurance is the percentage you split with your insurer after the deductible is met. Together, they determine your real cost of care — not just your monthly premium.

Once you understand how these pieces fit together, choosing a health plan becomes far less intimidating. You can evaluate plans with confidence, budget more accurately for medical expenses, and avoid unwelcome surprises when a bill arrives. The goal of health insurance is financial protection — and knowing your cost-sharing terms is the first step to making it work for you.